DFDS and Finnlines were least exposed, while Color Line and Tallink Silja got a real blow in the first half of the year with the pandemic

DFDS came out of the corona-affected first half of 2020 better than other major shortsea and ferry operators in Northern Europe.

While the Danish shipping company had to note a decrease in turnover of 19 percent, which in itself is dramatic, but gracious in relation to two of the Scandinavian/Baltic colleagues in the industry in particular. Norwegian Color Line experienced a half-year in which revenue was halved with a decrease of 51 percent from 219 million euros in 2019 to 107 million euros in 2020. Estonian Tallink Silja experienced a decrease in revenue of 49.5 percent from 435 million euros. In comparison, DFDS’s revenue in the period fell from 1.1 billion euros in the first half of 2019 to 888 million euros this year.

However, it is not possible to compare the Northern European ferry and shortsea operators one-on-one. This is partly because the shipping companies have different geographical distribution and are relatively different in relation to the market mix between e.g. cruise ferry, ro/pax and ro/ro.

DFDS’s significantly larger turnover must be seen in the light of the fact that the company, unlike the other Northern European shipping companies today, also has a large operation in the Mediterranean. However, with the nature of the pandemic, its global presence and its consequent global impact, the geographical spread of the markets does not necessarily disturb the basis of comparison.

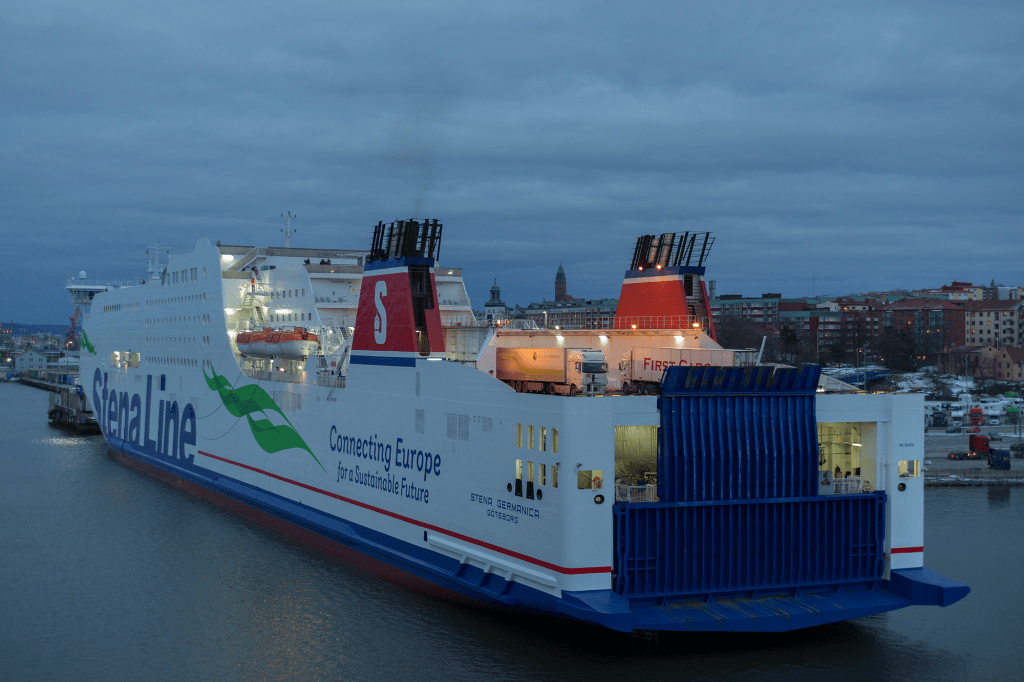

Two of the other major Northern European players that can be compared to DFDS are Swedish Stena Line and Finnish Finnlines, the latter currently owned by the Italian Grimaldi group. In the first half of the year, Stena Line experienced a decrease in revenue of 25 percent. In the first six months of 2019, it was 638 million euros, while it had fallen to 479 million euros in the half year 2020.

The impact on Finnlines with a decrease in revenue of 20 percent was almost on a par with DFDS. The drop in Finnlines’ turnover was from 296 million euros in the first half of 2019 to 236 million euros in the same period this year. Finnlines is the one of the major operators in Northern Europe, which can best be compared with DFDS based on the market mix.

About 63 percent of the fleet at Finnlines consists of ro/ro ships, (pure cargo ships). The figure at DFDS is around 67 percent including the company’s side port vessels but excluding chartered-in container vessels. The percentage for ro/pax, (freight-oriented passenger ships), is also relatively close between the two shipping companies. At Finnlines it is 37 percent, while at DFDS it is 26 percent, including the large “day ferries” on the English Channel.

The big difference between the Danish and Finnish shortsea operator is on cruise ferries. The larger the share of the fleet that is made up of with this passenger-heavy segment, the harder the company has so far been affected by the corona pandemic, the overall picture shows.

But here, overall, DFDS has performed better than Finnlines, which otherwise, unlike DFDS, has not had to deal with laid-up cruise ferries, but still comes out of the half-year with a marginally larger drop in revenue than DFDS. 7 percent of the fleet at DFDS consists of cruise ferries, while all Finnlines’ passenger-carrying ships are of the more freight-oriented ro/pax type.

Stena Line, which is the world’s largest privately-owned ferry company, experienced a revenue drop of about 5 percentage points greater than the Danish and Finnish competitors. During the period, the Swedish shipping company has benefited from operating only a few of what can roughly be described as cruise ferries on corridor-like routes, where at the same time there is also a large continuous freight volume.

Otherwise, Stena Line’s passenger-carrying fleet must be described as a pronounced ro/pax fleet, corresponding to 77 percent. The remaining 23 percent are pure ro/ro ships. Therefore, it is also a significant leap up to the two far more cruise ferry-oriented shipping companies Color Line and Tallink Silja.

Tallink Silja’s market is on the Baltic Sea between the Estonian, Swedish, Finnish and Latvian capitals with the Åland Islands as a main hub that enables tax-free sales on board. Most of the revenue is therefore gained above the car decks, so to speak.

That is, from on-board sales and service, while only a lesser part of the routes is based on trailer freight and transport passengers between the four countries. Therefore, the Tallink Silja fleet consists of as much as 64 percent cruise ferry tonnage, while the remaining ships are all ro/pax ferries.

Color Line is the high jumper in relation to falling revenue and has approx. 58 percent of the fleet tied up in the cruise ferry market. The cruise ferries on the Oslo – Kiel route, which is the world’s largest of its kind, have been laid-up for a long time during the half year, while the route’s third ship, Color Line’s only ro/ro ship, solely has maintained the direct freight corridor between Norway and Germany.

However, a large part of Norway’s freight to and from the continent also transits Hirtshals in Denmark. Throughout the six months, Color Line has maintained daily freight capacity with one of the company’s ro/pax ferries. The worst affected, however, is the Norwegian shipping company’s cruise ferry route between Sandefjord and Strømstad, where the vast majority of revenue is derived from tax-free onboard sales.

Both ships on the route, one of which is a newbuilding, are here in the third quarter of the year still laid-up in Sandefjord.

| MILLION EUR | H1 2020 | H1 2019 |

| DFDS | ||

| Revenue | 888 | 1,090 |

| EBITDA | 150 | 224 |

| Color Line | ||

| Revenue | 107 | 219 |

| EBITDA | -18 | 28 |

| Tallink/Silja | ||

| Revenue | 220 | 435 |

| EBITDA | 1.2 | 54.5 |

| Stena Line | ||

| Revenue | 479 | 638 |

| EBITDA | 49.8 | 133 |

| Finnlines | ||

| Revenue | 236 | 296 |

| EBITDA | 66.4 | 83.5 |

Meget smukke fotos Søren spændende view

Peter

LikeLiked by 1 person